Machine Learning, P-values and Confidence Intervals

How do you know your ML results aren’t due to chance?

In hypothesis testing, scientists use p-values and confidence intervals to make sure their observations are not due to chance. Can we do something similar in ML?

In machine learning, data scientists generally look at out-of-sample validation to determine the fitness of a model. But can we test specifically if the model is picking up relationships that are really there, or are only there by chance?

I think this would be valuable in situations where you have very wide datasets with many columns and few samples, or if you are modeling on small datasets generally, for example if you don’t have enough data for a test set.

I used the titanic dataset on kaggle to explore this idea.

The first step is to get the training set and get it ready for modeling.

#Get Train Set Ready *******

Boat <- read.csv("train.csv")

#Title and Last Name

Boat$title<- word(Boat$Name,1, sep = fixed('.'))

Boat$title<- word(Boat$title,-1)

Boat$lastName <- word(Boat$Name, 1)

##Embarked

Boat$Embarked[Boat$Embarked == ""] <- "C"

##Remove

Boat$Ticket <- NULL

Boat$lastName <- NULL

TrainID <- Boat$PassengerId

Boat$PassengerId <- NULL

Boat$Name <- NULL

##Factors

Boat$Sex <- as.numeric(Boat$Sex)

Boat$Pclass <- as.factor(as.numeric(Boat$Pclass))

##Age

Boat$Age[is.na(Boat$Age)] <- median(Boat$Age, na.rm = TRUE)

Boat$Fare[is.na(Boat$Fare)] <- median(Boat$Fare, na.rm = TRUE)

##Title

Boat$title2[Boat$title == "Lady" |

Boat$title == "Countess" |

Boat$title == "Don" |

Boat$title == "Dr" |

Boat$title == "Rev" |

Boat$title == "Sir" |

Boat$title == "Johnkheer"] <- "Rare"

Boat$title2[Boat$title == "Major" |

Boat$title == "Countess" |

Boat$title == "Capt"] <- "Officer"

Boat$title2[is.na(Boat$title2)] <- "Common"

Boat$title2 <- NULL

Boat$Cabin <- NULL

#write.csv(Boat, file = "trainboat_fin.csv")

I ran an xbgTree algorithm on the training data.

#Rmodel*****************

set.seed(1)

xbg <- train(factor(Survived) ~.,

method = 'xgbTree',

data = Boat); print(xbg)

The confusion matrix shows the model has an overall accuracy ~ 83%.

confusionMatrix(xbg)FALSE Bootstrapped (25 reps) Confusion Matrix

FALSE

FALSE (entries are percentual average cell counts across resamples)

FALSE

FALSE Reference

FALSE Prediction 0 1

FALSE 0 54.8 10.1

FALSE 1 7.1 28.0

FALSE

FALSE Accuracy (average) : 0.828

This is where it get’s interesting…

So I have a basic model that I ran on a famous dataset, now what?

I want to be able to examine whether or not the modeling is accurate by chance. On approach that comes to mind is to randomize the dataset and rerun it through the algorithm.

##Perturb Data *****

Boat_random <- Boat

Boat_Label <- Boat$Survived

Boat_random$Survived <- NULL

Boat_random = as.data.frame(lapply(Boat_random, function(x) { sample(x) }))

Run the randomized dataset through the original model.

The data in this case is randomized, meaning that the columns do not contain information regarding the target. The model performance should degrade in response this randomization.

random_pred <-predict(xbg, Boat_random, type="prob")

random_pred2 <-predict(xbg, Boat_random)

Let’s take a look at the confusion matrix.

The confusion matrix shows an accuracy of ~53%

random_pred2 <- as.factor(random_pred2)

Actual <- as.factor(Boat_Label)

confusionMatrix(Actual, random_pred2)FALSE Confusion Matrix and Statistics

FALSE

FALSE Reference

FALSE Prediction 0 1

FALSE 0 367 182

FALSE 1 232 110

FALSE

FALSE Accuracy : 0.5354

FALSE 95% CI : (0.502, 0.5685)

FALSE No Information Rate : 0.6723

FALSE P-Value [Acc > NIR] : 1.00000

FALSE

FALSE Kappa : -0.0102

FALSE

FALSE Mcnemar's Test P-Value : 0.01603

FALSE

FALSE Sensitivity : 0.6127

FALSE Specificity : 0.3767

FALSE Pos Pred Value : 0.6685

FALSE Neg Pred Value : 0.3216

FALSE Prevalence : 0.6723

FALSE Detection Rate : 0.4119

FALSE Detection Prevalence : 0.6162

FALSE Balanced Accuracy : 0.4947

FALSE

FALSE 'Positive' Class : 0

FALSE

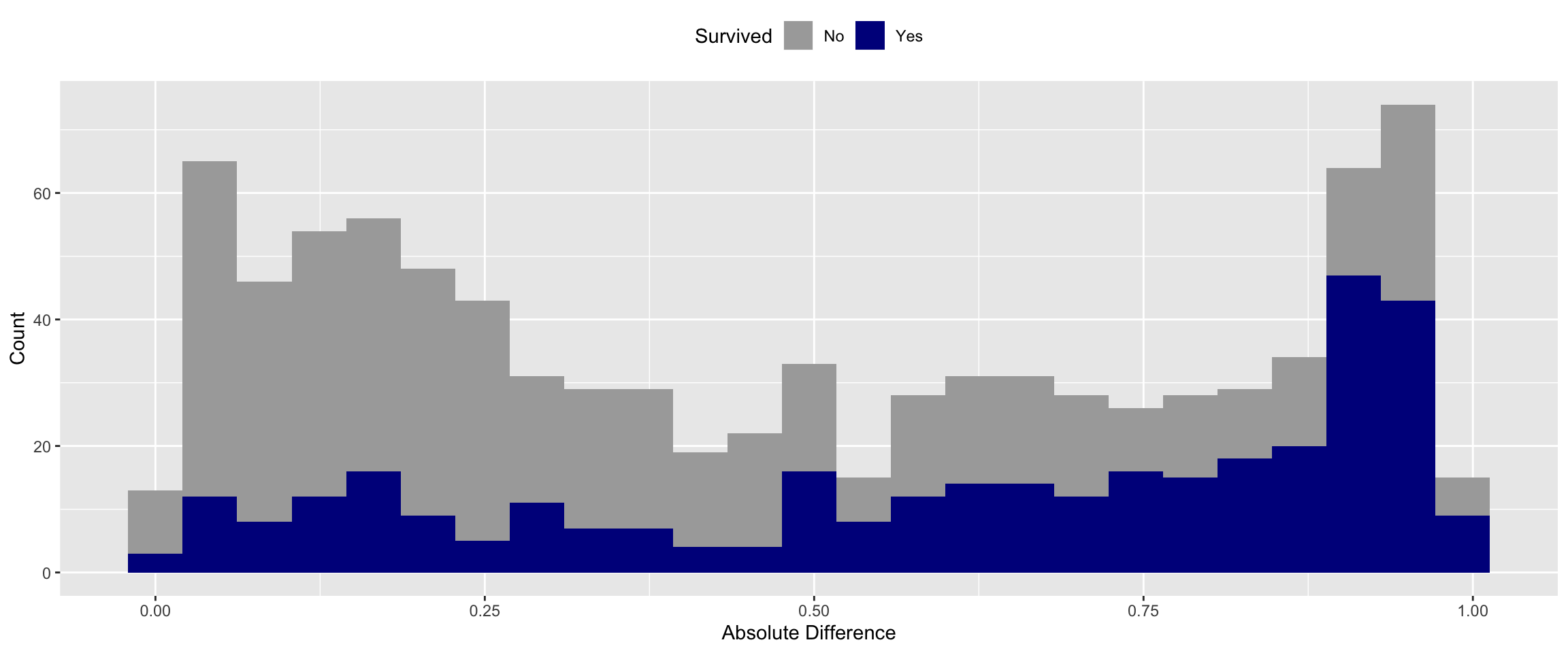

Next I wanted to see the error distribution of the random model.

The model shouldn’t predict well because there are no real relationships in the data. However, it should get some right just by chance. I used a simple difference metric to evaluate the fitness of the model. Specifically, I subtracted the predicted probability by the actual value (0 or 1). I then took the median of the absolute difference.

Boat_random$Actual <- Boat_Label

Boat_random$Random_Pred <- random_pred[,2]

Boat_random$Survived[Boat_random$Actual == 1] <- "Yes"

Boat_random$Survived[Boat_random$Actual == 0] <- "No"

Boat_random$diff <- Boat_random$Actual - Boat_random$Random_Pred

Boat_random$diff_abs <- abs(Boat_random$diff)

median(Boat_random$diff_abs)FALSE [1] 0.4612427

With random data the median error of the model is ~46%.

You can see above that the algorithm did not predict well for either class when the data was randomized.

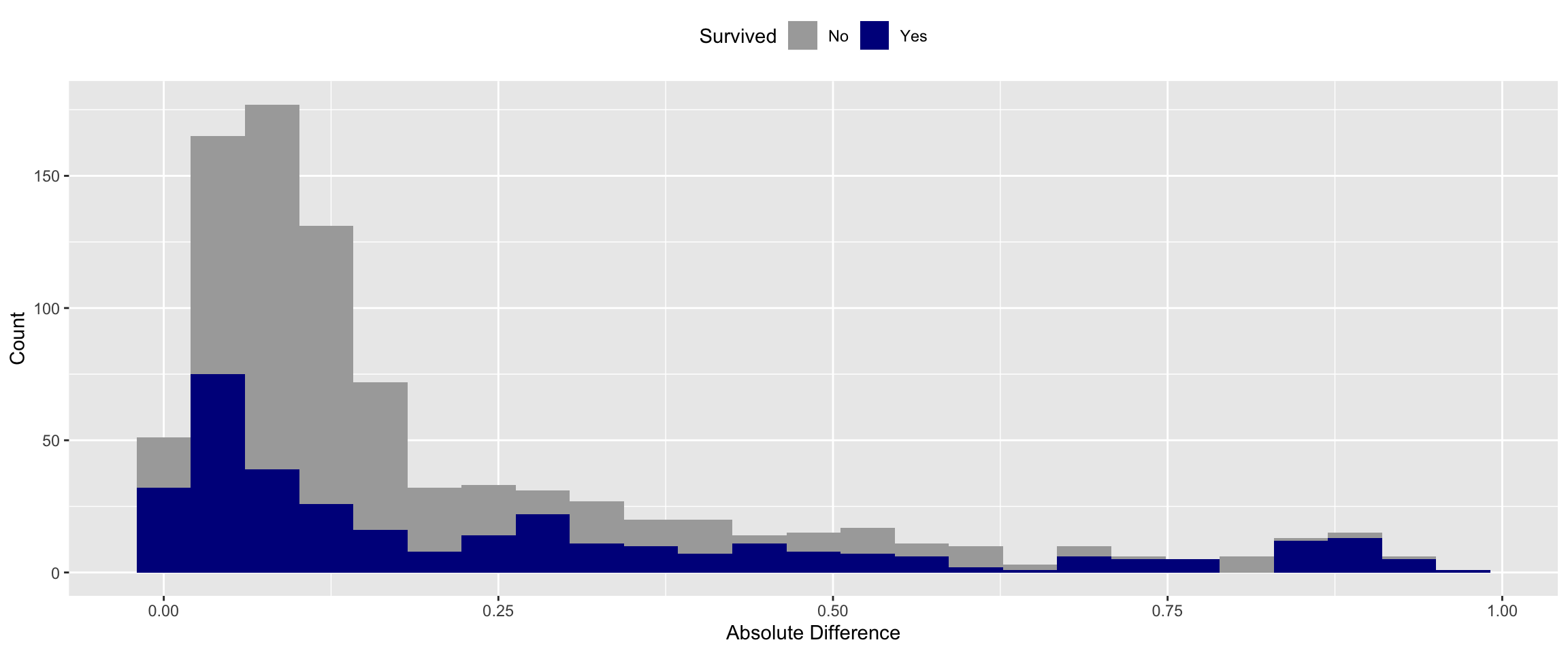

In order compare apples to apples, I ran the training data through the model again as well.

With meaningful data the median error of the model is only ~11%. This is a large reduction of error compared to model that predicted on random data. This is a good sign that our model is picking up relevant patterns.

#Predict on training data for comparison**********

boat_training_exp <- Boat

survived <- boat_training_exp$Survived

boat_training_exp$Survived <- NULL

real_pred <-predict(xbg, boat_training_exp,type="prob")

boat_training_exp$prediction <- real_pred[,2]

boat_training_exp$actual <- survived

boat_training_exp$diff <- boat_training_exp$actual - boat_training_exp$prediction

boat_training_exp$diff_abs <- abs(boat_training_exp$diff)

median(boat_training_exp$diff_abs)

There is a reduction in error of the predictions when I add meaningful vs. random data. But this doesn’t address whether or not this decrease is due to chance

I decided can borrow a concept from non-parametric statistics and use a wilcoxon-signed-rank test to compare the distributions of absolute errors (random vs. training). I chose this test because it relies on medians rather than means, so it does not assume a normal distribution.

wilcoxon_data = data.frame(Random= Boat_random$diff_abs, Training=boat_training_exp$diff_abs)

res <-wilcox.test(wilcoxon_data$Training, wilcoxon_data$Random)

resFALSE

FALSE Wilcoxon rank sum test with continuity correction

FALSE

FALSE data: wilcoxon_data$Training and wilcoxon_data$Random

FALSE W = 189736, p-value < 0.00000000000000022

FALSE alternative hypothesis: true location shift is not equal to 0

The results show that the p-value is very small (0.00000000000000000000), meaning that we can with reasonable credibility assert that the reduction in error that we see with our XBGTree model predicting on real vs. random data is likely not due to chance.

What about confidence intervals?

P-values are nice, but they are not especially useful on their own. Confidence intervals would be a big boost to my confidence in the differences.

I used another non-parametric approach to calculate these as well. Specifically, I used a bootstrapping technique and took 1000 random samples from the random and training absolute error and calculated the median for each of those random samples.

bootstrap_data = data.frame(Random= Boat_random$diff_abs, Training=boat_training_exp$diff_abs)

med.diff2 <- function(data, indices) {

d <- data[indices] # allows boot to select sample

return(median(d))

}

# bootstrapping with 1000 replications

results_training <- boot(data=bootstrap_data$Training, statistic=med.diff2, R=1000)

results_random <- boot(data=bootstrap_data$Random, statistic=med.diff2, R=1000)

#kable(results_random)

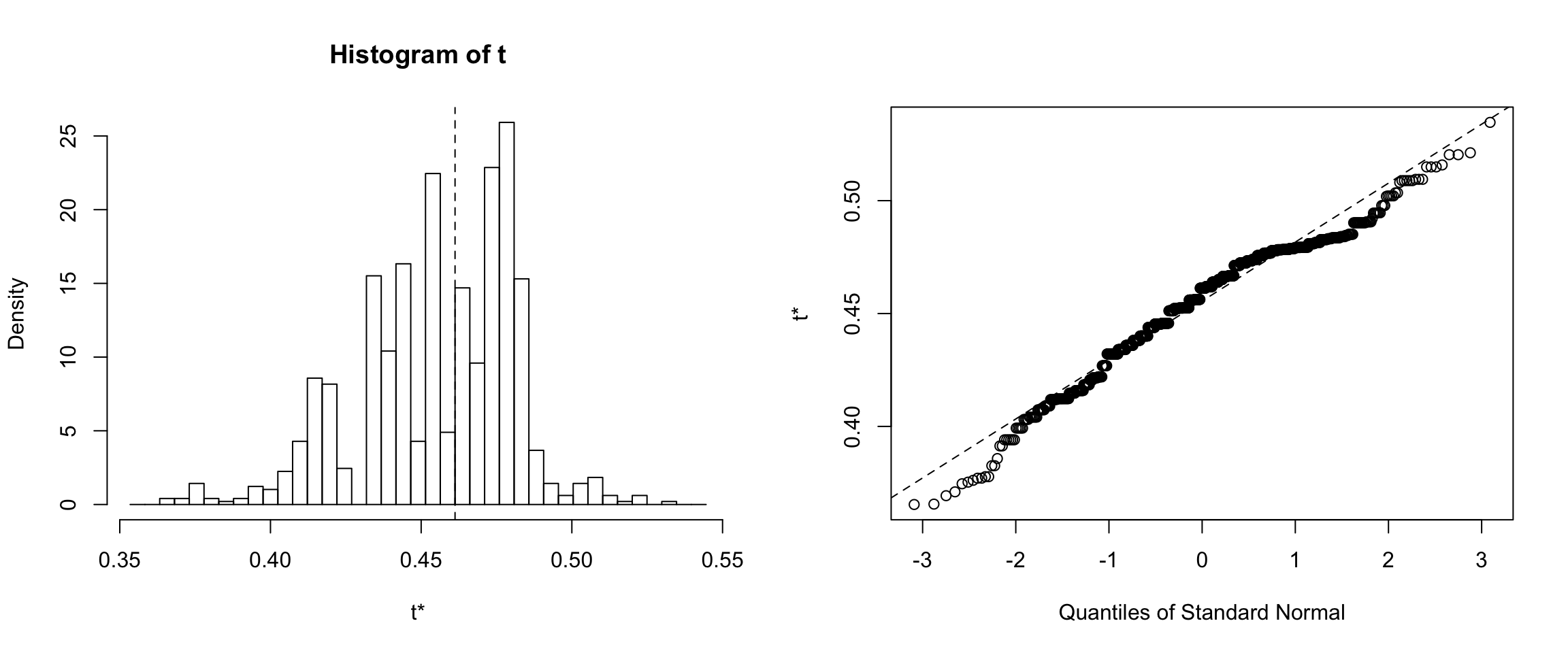

Results for the Training dataset

Results for the non-random training dataset showed that 95% of the medians calculated from 1000 bootstrapped error samples are between ~10% and ~12%.

Confidence intervals for Training dataset

# get 95% confidence interval

tci <- boot.ci(results_training, type=c("norm"))confidence interval is: 95.0%, 10.3%, 12.1%

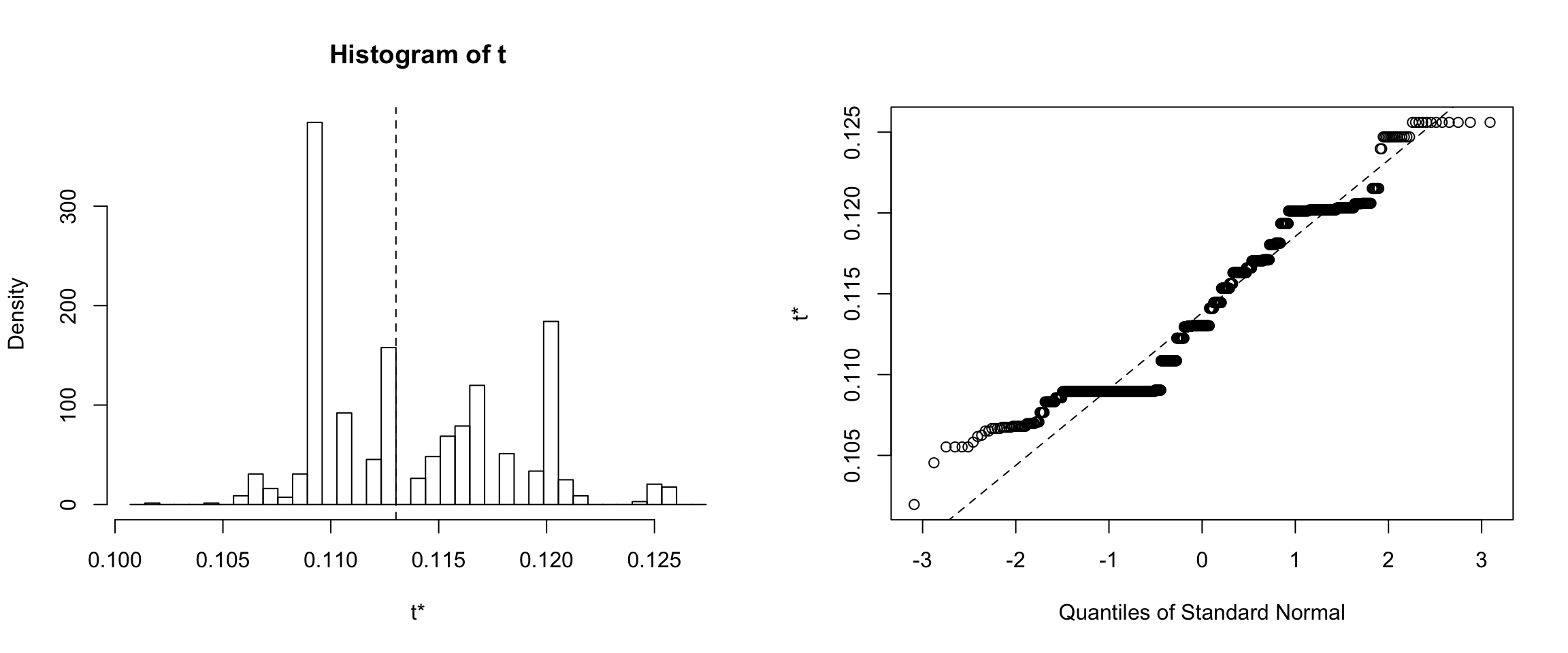

Results for the Random dataset

Results for the random dataset showed that 95% of the medians calculated from 1000 bootstrapped error samples are between ~42% to ~52%.

Confidence intervals for Random dataset

# get 95% confidence interval

rci <-boot.ci(results_random, type=c("norm"))

confidence interval is: 95.0%, 41.6%, 51.8%

Do the p-values decrease smaller samples sizes? Do confidence intervals increase?

It is important to see if these metrics degrade with smaller sample sizes. If so, then this logic may actually be a good measure of whether or not your modeling results are due to chance. With smaller datasets one should be less confident. I decided to create learning curves using p-values and confidence intervals for the random and non-random data. Specifically, I created 4 segments of each.

- 10% of the data

- 25% of the data

- 50% of the data

- 100% of the data

P-value learning curves

You can see below that the p-value gets smaller as the data size increases.

#Get p-values for each dataset size

wilcoxon_data_10per = sample_n(wilcoxon_data, 89)

wilcoxon_data_25per = sample_n(wilcoxon_data, 223)

wilcoxon_data_50per = sample_n(wilcoxon_data, 445)

wilcoxon_data_100per = wilcoxon_data

res_10 <-wilcox.test(wilcoxon_data_10per$Training, wilcoxon_data_10per$Random)

res_25 <-wilcox.test(wilcoxon_data_25per$Training, wilcoxon_data_25per$Random)

res_50 <-wilcox.test(wilcoxon_data_50per$Training, wilcoxon_data_50per$Random)

res_100 <-wilcox.test(wilcoxon_data_100per$Training, wilcoxon_data_100per$Random)

learning_p <- data.frame("Pvalues" = c(res_10$p.value, res_25$p.value, res_50$p.value, res_100$p.value), "Segment" = c( "G_10%","G_25%","G_50%","G_100%"))

learning_p <- as.data.frame(learning_p)

learning_p2 <- select(learning_p, Segment, Pvalues)

kable(learning_p2, digits = 85)| Segment | Pvalues |

|---|---|

| G_10% | 0.0000003051927387954484036276803227138998408918268978595733642578125000000000000000000 |

| G_25% | 0.0000000000000000000000977534287158965961818476023791949230067169776689644789647399767 |

| G_50% | 0.0000000000000000000000000000000000000030721892676219230904894423043585917266578170005 |

| G_100% | 0.0000000000000000000000000000000000000000000000000000000000000000000000000000000038375 |

Bootstrapping

I applied the same bootstrapping principles to the small dataset as well.

small_data <- boat_training_exp

colnames(small_data)[colnames(small_data)=="diff_abs"] <- "train_diff"

small_data$random_diff <- Boat_random$diff_abs

small_data_10 <- sample_n(small_data, 89)

small_data_25 <- sample_n(small_data, 223)

small_data_50 <- sample_n(small_data, 445)

small_data_100 <- small_data

# bootstrapping with 1000 replications

results_training_10 <- boot(data=small_data_10$train_diff, statistic=med.diff2, R=1000)

results_training_25 <- boot(data=small_data_25$train_diff, statistic=med.diff2, R=1000)

results_training_50 <- boot(data=small_data_50$train_diff, statistic=med.diff2, R=1000)

results_training_100 <- boot(data=small_data_100$train_diff, statistic=med.diff2, R=1000)

results_rand_10 <- boot(data=small_data_10$random_diff, statistic=med.diff2, R=1000)

results_rand_25 <- boot(data=small_data_25$random_diff, statistic=med.diff2, R=1000)

results_rand_50 <- boot(data=small_data_50$random_diff, statistic=med.diff2, R=1000)

results_rand_100 <- boot(data=small_data_100$random_diff, statistic=med.diff2, R=1000)

Bootstrapping Curves

The median errors from the bootstrapping sample reduce with the addition of more data.

Confidence intervals for the different datasets

# get 95% confidence interval

tci_10 <-boot.ci(results_training_10 , type=c("norm"))

tci_25 <-boot.ci(results_training_25 , type=c("norm"))

tci_50 <-boot.ci(results_training_50 , type=c("norm"))

tci_100 <-boot.ci(results_training_100 , type=c("norm"))

tci2 <- as.data.frame(rbind(tci_10$normal, tci_25$normal, tci_50$normal, tci_100$normal))

tci2$Segment <- c("S_10%", "S_25%","S_50%", "S_100%")

tci2$median <-c(tci_10$t0, tci_25$t0, tci_50$t0, tci_100$t0)

tci2$group <- "training"

rci_10 <-boot.ci(results_rand_10 , type=c("norm"))

rci_25 <-boot.ci(results_rand_25 , type=c("norm"))

rci_50 <-boot.ci(results_rand_50 , type=c("norm"))

rci_100 <-boot.ci(results_rand_100 , type=c("norm"))

rci2 <- as.data.frame(rbind(rci_10$normal, rci_25$normal, rci_50$normal, rci_100$normal))

rci2$Segment <- c("S_10%", "S_25%","S_50%", "S_100%")

rci2$median <- c(rci_10$t0, rci_25$t0, rci_50$t0, rci_100$t0)

rci2$group <- "random"

conf_int <- rbind(tci2, rci2)

conf_int$ci_l <- conf_int$median - conf_int$V2

conf_int$ci_h <- conf_int$V3 - conf_int$median

conf_int$Segment = factor(conf_int$Segment, level = c("S_10%", "S_25%","S_50%", "S_100%"))

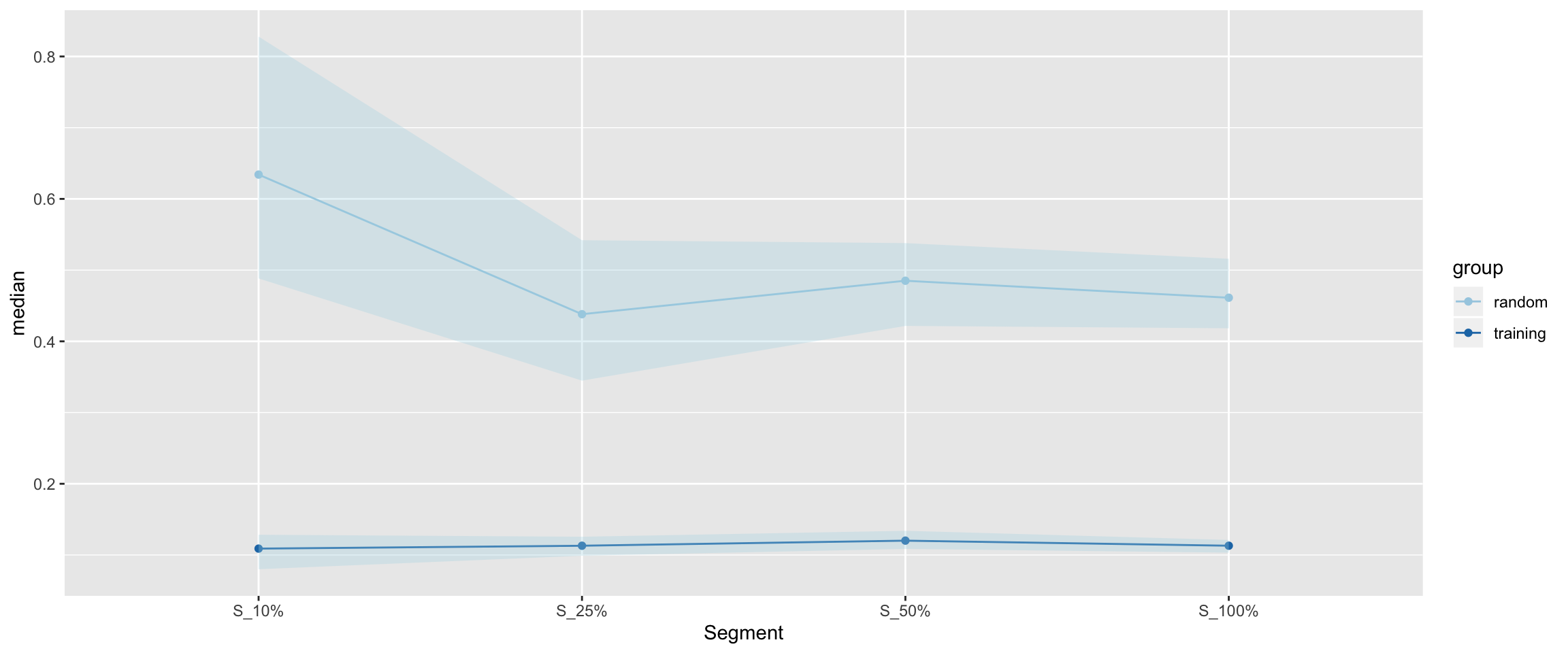

Median error and CI for non-random and random data.

There seems to be a point of diminishing/reversal of returns for the random dataset. The training dataset has a bit of a floor effect, but the confidence intervals do shorten with the addition of more data as well.

Table of confidence intervals.

conf_table <- select(conf_int, Segment = Segment, group, median, 'Low_95%' = V2, 'High_95%' = V3)

conf_table$length <- conf_table$`High_95%` - conf_table$`Low_95%`

kable(conf_table, digits = 3)| Segment | group | median | Low_95% | High_95% | length |

|---|---|---|---|---|---|

| S_10% | training | 0.109 | 0.080 | 0.128 | 0.048 |

| S_25% | training | 0.113 | 0.099 | 0.126 | 0.027 |

| S_50% | training | 0.120 | 0.109 | 0.134 | 0.025 |

| S_100% | training | 0.113 | 0.103 | 0.121 | 0.018 |

| S_10% | random | 0.634 | 0.488 | 0.828 | 0.340 |

| S_25% | random | 0.438 | 0.345 | 0.542 | 0.197 |

| S_50% | random | 0.485 | 0.422 | 0.538 | 0.116 |

| S_100% | random | 0.461 | 0.418 | 0.516 | 0.098 |

Summary

I created an XGBTree model with the caret package on the Titanic dataset with about ~83% accuracy.

When I ran a randomized dataset through the model the accuracy dropped by quite a lot to ~53%.

I calculated the differences between the predicted and actual values simply by subtracting the probability of surival by the class (0 or 1) and taking the absolute value. I then calculated the medians.

The median errors for the random data: 46.1%

The median errors for the non-random data: 11.3%

Then I plotted the distributions of these errors for the random and non-random samples.

In order to see if the differences were due to chance I ran the median error for each sample through a Wilcoxon sign ranked test - which is a way to compare non-normal distributions. This test determined that these error distributions are significantly different from one another: p-value: 0.00000000000000000000.

After finding the p-vlaue I used a non-parametric bootstrapping method to calculate confidence intervals.

The confidence intervals in the non-random data (95.0%, 10.3%, 12.1%) are lower than the random data (95.0%, 41.6%, 51.8%), further supporting that these two distributon of errors do not have much overlap.

- Finally, I tested whether or not this method would be impacted by sample size. Confidence in findings should theoretically decrease with smaller samples, so I took a random sample of 10%/25%/50%/100% of the data and recalculated learning curves for each metric.

Discussion

I set out to try and apply some of the validation metrics used in statistics to machine learning. The idea is certainly not totally there, but I think this process is a good start to marrying two fundamental concepts between statistics and machine learning.

The p-values and confidence intervals scale down in a way that makes sense with a smaller dataset.

Some other ideas:

Instead of using an absolute error, this could be refined by doing the same process with a metric like LogLoss - which has some interesting properties on it’s own.

Using non-parametric comparisons make sense if you don’t know the distribution of the data, but what if you do?

Maybe running one random permutation isn’t enough, are there concepts that can be borrowed from Montecarlo simulations? Or is this just extra work without any benefit?

I ran a random sample as well as the training sample through the dataset, but I did not use the test sample (mostly because the results are not available).